A brick tax was first proposed in 1756 but was rejected and again in 1778. However, at the end of the War of American Independence in 1784, a tax on bricks and tiles was introduced by Mr Pitt to cover the cost of the war. Originally the charges were 2s. 6d. per 1000 for bricks, plain tiles 3s per 1000. Pan or ridge tiles 8s per 1000, paving tiles less than 10 inches square 1s 6d. per 100, paving tiles greater than 10sq inches 3s per 100. All other tiles 3s. per 1000. The tax was levied on the fresh made brick or tile before they were burnt, therefore any bricks that were over burnt already had the tax paid on them, there was a 10% allowance for this.

The revenue was protected by branding the interior of the mould with the word ” Excise,” so as to impress the brick.

In 1794 the tax was increased to 4s. per 1000 and in 1797 to 5s. Originally as the tax was levied on the number of bricks there was a drive to make bricks bigger, allowing more ‘brick’ to be made per unit of tax. The treasury countered this by introducing a size bar by an act in 1803. This stipulated any brick bigger than 10 ins by 5 ins. Were charged double duty. This measurement was of the brick fresh from the mould and so the burnt bricks would be smaller due to shrinkage.

In 1805 the tax was increased to 5s. 10d. per 1000 at which level it stayed until the repeal of the tax.

In 1826 after a great deal of protest and pressure, field drains were exempted from tax provided they had the word ‘DRAIN’ impressed. (In 1850 the tax was abolished altogether.

Hence drainage pipes marked ‘drain’ can be safely dated c.1826 to c.1850)

In 1839 the size of the brick was altered to one of volume with a limit of 150 cu ins. To allow the development of different shaped bricks.

It may be added that bricks for building, repairing or enlarging churches were not charged with duty.

The brick tax repealed in 1850.

Below – 08/09/1784 – Caledonian Mercury – Details of which products are taxed.

.

13/06/1801 – Caledonian Mercury – Mr Vanittart moved for a committee on tomorrow to take into consideration the expediency of raising the tax on bricks and tiles, in proportion to dimensions as the tax on those articles had of late been considerably extended by making them in general larger sizes than usual …

Below – 17/04/1823 – Inverness Courier – An in-depth article about the brick tax and how it affects the stone and slate industry too. Only a small section is reproduced here.

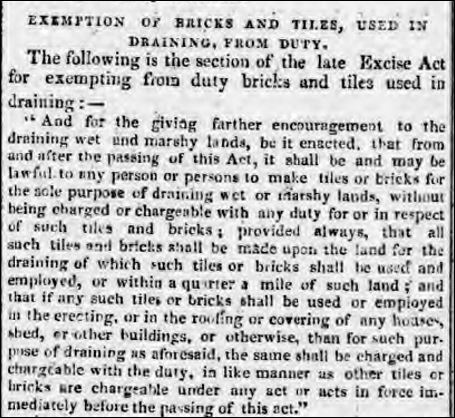

Below – 19/07/1824– Caledonian Mercury – Exemption of bricks and tiles used in draining from duty.

Below – 29/07/1824 – Inverness Courier – Exemption of bricks and tiles used in draining from duty. Exemption of bricks and tiles, used in draining, from duty.

The following is the section of the late Excise Act for exempting from duty bricks and tiles used in draining:-

” And for the giving farther encouragement too the draining wet and marshy lands, be it enacted, that from and after the passing of this Act, it shall be and maybe lawful to any person or persons to make tiles or bricks for the sole purpose of draining wet or marshy lands, without being charged or chargeable with any duty for or in respect of such tiles and bricks, provided always, that all such tiles and bricks shall be made upon the land for the draining of which such tiles or bricks shall be used and employed, or within a quarter a mile of such land; and that if any such tiles or bricks shall be used or employed in the or in the roofing or covering of any houses, shed, or other buildings, or otherwise, than for such purpose of draining as aforesaid, the same shall be charged and chargeable with the duty, in like manner as other tiles or bricks are chargeable under any act or acts in force immediately before the passing of this act.”

Below – 24/02/1831 – Fife Herald – Issues regarding brick size and stating the brick tax should be repealed.

Below – 13/07/1831 – Aberdeen Press and Journal – Glasgow and West of Scotland brickmakers agree to petition the Govt to repeal the brick tax.

05/05/1832 – Edinburgh Evening Courant – Farmers and others should aware that any person or persons can make bricks or tiles for the purposes of draining, free from duty, provided the word “drain” be stamped on them. But any individual using the same for any other purposes besides draining, subjects himself to a penalty of L. 50. (£50).

Below – 01/05/1833 – The Scotsman – Alexander Bald, Alloa brick and tileworks writes to the Government with a plea to repeal the brick tax.

Below – 18/04/1834 – Stamford Mercury –

19/10/1839 – Durham Chronicle – Repeal of duty on bricks used for draining land. An act consolidating and making other alterations in the laws imposing duties on bricks which received the Royal Assent on the 19th July, contains the following clauses and whereas it is expedient to exempt from the duties by this act imposed bricks made for thy sole purpose of draining wet and marshy land, it therefore enacted, that it shall be lawful for any person to make brick for sole the purpose of draining wet and marshy lands without being charged or chargeable with any duty for or in respect of such bricks, all such bricks being in the making thereof stamped or moulded with the word “drain” in or near the centre of the surface of such bricks, in so plain and distinct a manner that the same may be easily and clearly legible to any of excise or other person examining the same both before and after such bricks shall have gone through the process of burning and become fit for use, provided always, that it shall not be lawful for any person to employ or make use of any such bricks for any other purpose than in draining wet and marshy lands and constructing the necessary drains, gouts, culverts, arches, and walls of the brick-work proper and necessarily required for effecting and maintaining the drainage of such lands and every maker of such bricks or other person who shall sell or deliver or use employ any brick with the word “drain” so stamped or moulded thereon for any other purpose than aforesaid shall forfeit fifty pounds. And be it enacted, that no drawback shall be allowed payable on any bricks having the word “drain” stamped or moulded thereon, or any bricks which shall not be sound and unbroken, and well and perfectly made and manufactured, and worth at least the duties of excise charged thereon if sold for home consumption.

28/07/1847 – Dumfries and Galloway Standard – Wigtown 19th July. We had rather unusual importation of bricks, per the sloop Darnhale, Captain Epeson, from Belfast; and as no duty is paid for making bricks in Ireland, an import duty of 5s. 10d. is payable, per thousand, when they arrive in Scotland or England; and to charge this duty caused both the authorities of the custom-houses and excise to exert themselves.

Below – 08/09/1848 – Stamford Mercury – Excise Prosecution. The Queen v. Rd.Knight. —At the petty sessions for the soke of Peterboro’ held on Saturday last, (before the Rev. W. Strong, chairman, T. Atkinson, Esq., and the Rev. John Hopkinson,) Mr Rd. Knight, a draper, of Stamford, appeared to on information laid against him by the officers of excise. The Information was the name of Wm. Wardle, and it charged that on the July last certain brick-yard at Helpstone of which Mr Knight is proprietor, 540 bricks were taken to the kiln to be burnt before they had been properly charged with the excise-duty. Mr Phillips, of the firm of Thompson, Son, and Phillips, of Stamford, appeared for the defendant, and stated that upon an investigation of the matter he could not deny that his workmen had been guilty of an irregularity and that consequently, he (Mr Knight) was liable to a penalty; but in order that the facts of the case might come fully before the bench, it was intended to enter a plea of not guilty. Mr Forbes, the collector of excise for the Stamford district, then stated the case. He said that an officer went on a certain day to Mr Knight’s brick-yard, and numbered some rows of bricks, one of which was numbered 4. He made several subsequent surveys, and on the 17th July, he found that No. 4 hack had been removed to the kiln without being charged. In preparing bricks for the kiln, they were sometimes put in rows and sometimes on flats: in Mr Knight’s yard they were put in rows called, hacks, and when in this state it was customary for the excise officer to enter them and charge the bricks with the proper duty. When it was found that No. 4 hack had been taken away without being charged, the foreman at the yard said it was a mistake. He (Mr Forbes) did not know whether would appear in evidence, but it was stated that Mr Knight knew nothing of the matter that it had been done to evade the duty, It could not benefit Mr Knight, as the men who had the management of the yard did not stand exactly in the relation of servants, they being contractors to make bricks at so much per thousand; but whether that was the fact or not, Mr Knight was entered as the proprietor of the yard, and he was responsible to the excise for any infringement of the revenue. Mr Forbes then minutely described the circumstances they were afterwards detailed in evidence and called Chas. Knowles, the informer, who deposed that he surveyed Mr Knight’s yard at Helpstone from the 22d June to the 2d August. On the 15th July found No.4 hack five bricks high, and when he went again on the 17th, he found the hack all gone, It not having been charged or requested to be charged.—ln cross-examination, the witness stated that when he spoke to the men about it they said it was a mistake, that they thought the hack had been charged, and they requested him to charge it then, telling him how many bricks were in the hack at the time it was removed. He was further cross-examined at great length, to prove that be had circulated rumours in Stamford prejudicial to Mr Knight: he denied that he had done so, or that he had ever said he had watched all night in the corn, or that had ever seen Mr Knight in the brick-yard assisting in the removal of bricks. He said he had seen some irregularities in the yard, and had told the men of it, but what he meant by watching the yard was looking about him when he went to survey. Mr Phillips was proceeding with the cross-examination on points connected with aspersions on Mr Knight’s character by the witness when Mr Forbes interposed and said Mr Knight’s character stood too high to be affected by such reports. Mr Hy. D. Rix, the supervisor of excise, deposed that he was informed of the removal of hack No. 4, and went and found it as represented. On acquainting Mr Knight with what occurred, he said knew nothing about it and that the excise-officers were welcome to inspect his books, and he would give them all Information be could. The amount of duty on the 540 bricks would be something more than three shillings. Mr Phillips said the defendant did not deny the charge with the view of saving himself from the penalty, but to vindicate his character from reports that he himself had been cognisant of the removal of the bricks. Mr Knight had let the brick-yard to two men named Seymour and Cottingham, who provided with everything necessary to carry on the manufacture. The arrangement was that they should pay for labour and the duty, and Mr Knight then paid so much per thousand for the bricks when they were ready for sale. The removal of hack No. 4 was, as he was assured, quite a mistake, which occurred in this way- Seymour and Cottingham were setting the kiln, and a young man named Fell and woman were supplying them with bricks from the hacks for that purpose. Fell had got all the bricks from one part of the yard, and they then sent him to another where hack No.4 was situated. The lad, instead of taking bricks from No. 5 only (which had been charged), took them likewise from No. 4, and Seymour and Cottingham did not find out the blunder till nearly the whole of the hack had been removed when it was too late to replace it. Under those circumstances, he thought the Bench would mitigate the penalty to the lowest figure in their power; and an application would be afterwards made to the Board Excise for entire remission of the fine. He (Mr Phillips) was informed that the men who committed the mistake had been for many years in the brick-yard, and it was the first time they had committed such error. Seymour and Cottingham were then called to depose to facts: but both of them objected to being sworn, alleging that from their religious sentiments, they conscientiously objected to taking the oath, but would speak the whole truth. [Both men are members of Rev. Fred. Tryon’s congregation at Deeping.] Their testimony was consequently rejected. The lad named Fell, who removed the bricks, deposed that when he took them from hack No. 4, did not know anything about there not having been charged and that Seymour and Cottingham were setting the kiln, they could not tell where got them from. He said did not know that be had done wrong till the excise-officer afterwards questioned him about it The Magistrates then consulted, and decided upon mitigating the penalty from 50l. to 20l., that sum to include all costs. Mr Phillips asked their Worships whether they would object to countersign memorial for the remission of the entire penalty. The Chairman said he objected to do so on principle; and Mr Atkinson said the Board would infer, from the mitigation of the penalty, what the magistrates thought of the case. Mr Knight then paid the fine.

Below – 31/08/1849 – Dundee, Perth and Cupar Advertiser.

.

Below –

18/04/1850 – Abolition of brick duty – Culloden Tileworks price reduction.

Below – 05/12/1851 – The Glasgow Herald – Article regarding the lack of improvement in brick quality following the repeal of the brick tax.

Below – A drainage pipe found in Northumbria and marked ‘ Drain’ probably to ensure it avoided the brick tax.

.

Below – other examples of taxes on bricks.

1841 – 1842 -(page 55) River and Harbour dues. Tonnage, crane, weighing and shed dues, leviable on goods imported or exported at the Broomielaw. – Free for coals, bricks, tiles and slates, in bulk and in cask, except when vessels occupy a shed berth. Weighing duties to be paid by the owners, shippers or importers of goods, if required by the taxman or collector, appointed by the Trustees for ascertaining the River Tonnage, or other duties granted by this Act, provided the weight alleged by the skipper or importer of the goods be found less than the real weight, but, if equal to or greater than the real weight, the weighing duties to be paid by the Taxman or Collector. Weighing duties for coals to be paid only when weighed on the application of the owner or skipper. All articles, commodities, &c. except the under-mentioned, pay 1s. 4d. per ton – exemption – coals, bricks, lime, limestone, freestone, whinstone, manure, pantiles, etc. – 2d per ton

Below – Taxes were also levied for use of canals etc for brick transport eg

1851 – 1852 – Paisley – John Mitchell, collector, 43 High street. Leviable On Goods, Wares, Merchandise, Commodities, Cattle, Coals, and other things carried in or upon the River Cart, or Navigable Cut or Canal or any part thereof; and of the Duty on all Ships, Passage Boats, Barges, Lighters, Boats, or other Craft carrying any Passenger or Passengers upon the said River, or Navigable Cut or Canal, or any part thereof. – Each Ton of Fire-clay, Sand, Lime, and Bricks, – 4d. – (see link for full details of other taxes etc. that were levied at the time against other goods)

05/11/1904 – Peterhead Sentinel – Interesting reminiscences of Mr William Forbes – Mr Annan and Mr Havelock addressed a political meeting in Tipperty School near Ellon on Wednesday night. Mr William Forbes, Newark, who presided said in raising money to meet the enormous expenditure on the army, navy, interest on national debt, wars, etc., the Tory party had always favoured the method of indirect taxation, that was, putting duties or taxes on articles of consumption, in place of direct taxation, like the income tax, so that a man had great difficulty in ascertaining the exact amount of his contribution to the national revenue … Roofing tiles paid a duty of 7s per 1000, and years afterwards when he (the speaker) commenced to make bricks to build his first kiln in 1849 he had to give notice to the exciseman of his intention, submit his moulds for measurement, and if in any degree over the Government standard, double duty was charged on the bricks. The gauger visited the work twice a week to count the bricks made, and to facilitate his work they had to be built in exactly equal rows. When the collector came to Ellon he met him to pay 5s 10d per 1000 for all bricks in made whether saleable or lost by bad weather …